Asymmetry and Interdependence: India’s Economic Relations with China Post-2020

Abstract

Economic interests constitute a critical subset within the larger canvas of India–China bilateral relations. This subset has conditioned and shaped the relationship, which has been driven by perpetual mistrust and asymmetry. It is not an exaggeration to suggest that the economic component has prevented sustained, full-blown military conflict between the two major geopolitical rivals. In this context, this Occasional Paper explores the discourse on their economic relationship in the four years following the Chinese transgressions in Eastern Ladakh in the summer of 2020. It delves into the growing trade imbalance for India and its dependence on Chinese components, as well as skilled personnel, to support ‘Make in India’ ambitions. It also analyses the factors that compel China not to discount India in its economic and investment calculations. Finally, using labour relations as a framework to understand the evolving nature of economic development, the paper explains how the two countries are joined at the hip.

Keywords: India-China relations; trade balance; foreign direct investment; supply chains; labour; pandemic.

Economics has remained a distinct factor in the larger matrix of India–China bilateral relations, notwithstanding the troughs and crests that have characterised ties in other domains. While this has been the case since the rapprochement between the two countries in 1987, following the 1962 border conflict, it has become particularly salient in the last decade. It would not be out of place to say that the economic base now undergirds the superstructure of bilateral relations, to borrow Karl Marx’s formulation.[i] However, in this economic relationship, the balance of power has remained tilted in favour of China. Beijing’s upper hand in bilateral trade has been significant, while its non-tariff barriers—such as varying product standards, complex labelling requirements, opaque implementation of quality control orders, complex procedures in product registration, and delays in customs clearance—have stonewalled Indian access to the Chinese domestic market. India’s manufacturing ambitions, which have evolved over the last decade, are also heavily dependent on China for raw materials, components, machinery, and skilled personnel.

Exploring the complex and entangled economic relationship between India and China since Xi Jinping took over the reins of the Communist Party of China (CPC) in 2012, this Occasional Paper looks specifically into the discourse of the five years since the Chinese transgressions in Eastern Ladakh in the summer of 2020. The main focus is on the dynamics of Chinese capital in the Indian political economy. Beginning with the trade imbalance between the two countries, the paper examines the role of Chinese companies in India through a brief case study in the infrastructure and connectivity sector. It also turns its attention inwards, arguing that India must undertake economic and administrative reforms to confront the China challenge. This should not be limited to the central government but should involve pooling the strengths of industry, academia, and bureaucracy to better understand the ecosystem and to incubate ideas supported by financial resources and informed decisions. The analysis in this Occasional Paper is based on a textual review of Indian government documents, such as the Economic Survey and relevant budget related materials, supplemented by secondary literature. It also draws on select Chinese-language sources, including media reports and think tank analyses.

Emergence as Modern Nations: Common Yet Different Settings

India and China are the most populous countries in the world and have made strides in economic development as well as human capacities. Nation-state narratives about both countries have been dominated by their rising economic growth and global influence. These narratives, however, tend to obscure interesting convergences and parallels that offer possibilities for comparatively analysis, even though the two countries differ vastly in their political and social systems, as well as forms of social division. While India is riven with caste, religious and linguistic cleavages, China’s social divisions are largely along economic, political, and regional/spatial lines.

From inheriting largely rural, agrarian societies, to pursuing similar goals for their populations in terms of development and industrial modernisation, and the adoption of command planning strategies, there are interesting patterns of convergence between the two countries. Following market-oriented economic reforms, these similarities also extend to how they have ‘engaged in targeted interventions to provide safety nets for the poor’ (Duara and Perry 2018). At the same time, these points of convergence, and the ways in which the countries can be seen as mirror images of each other, offer possibilities for a closer examination of their governing practices and societal responses. This includes their political-economic journeys as modern nation-states beginning in 1947 and 1949, respectively; the role of the state and the adoption of public policies; economic transitions through the adoption of pro-market reforms; their intersection with global phenomena such as globalisation; and broader state–society relations.

However, despite the political and economic standing of both countries in the global order, bilateral relations have remained largely unstable, conditioned by increasing geopolitical competition and overshadowed by historical legacies and memories. The long-standing boundary dispute in the Himalayan region, which originates in the British colonial and Chinese imperial periods, continues to cast a long shadow in the contemporary period (Kalha 2014; Guyot-Réchard 2016; Rao 2021; Acharya 2022; Joshi 2022). The 1962 war between the two countries—where Tibet was also a key component (Stobdan 2019; Bhasin 2021)—was a turning point in shaping the future course of India–China relations. Mutual mistrust and animosity have since become default in this tenuous bilateral relationship, which continues to undergo its fair share of troughs and crests. The mode of conflict has also changed, from full-scale war to periodic low-intensity conflict between the two armies along the Line of Actual Control (LAC), often without shots being fired. This, coupled with rising geopolitical competition for markets, resources, and prestige, has further impacted the relationship.

Over the last decade, repeated ingress by the Chinese People’s Liberation Army’s (PLA) across the LAC has led to the mobilisation of troops and eyeball-to-eyeball confrontation in the arduous Himalayan terrain. The most long-standing of these occurred at multiple points in Eastern Ladakh in the summer of 2020 and lasted for four years. Unlike previous episodes, violence in the Galwan Valley during this conflict led to the loss of lives among troops on both sides. Notwithstanding this shift in the nature of conflict, India and China have sought to navigate their relationship, with economics becoming a central element of this process. Even amid oscillations between conflict and cooperation in India–China interactions over the years, the economic dimension has tempered hard-nosed politics and helped prevent escalation into real-time conflict.

The economic imperative was also an important factor in hastening negotiations to end the crisis in Eastern Ladakh, leading to the signing of the Patrolling Agreement between the two sides in October 2024. China remains indispensable to the offshore production of transnational corporations—despite all the chatter about diversification to newer geographies—and is therefore well integrated into global supply chains. Furthermore, China’s industrial capacities have increased exponentially, with domestic companies scaling up operations, beyond its borders, including in India. Cognisant of this economic and industrial dependence, China has increasingly leveraged its advantage over India. While economics— or rather, economic realities—may have prevented full-blown warfare, coercion on the wings of economic and industrial superiority is reshaping the terms of engagement and raising costs for Delhi, which has yet to find viable alternatives at scale.

China as a Benchmark: Ideational Wings for Ambitious Flights

China serves as something of a positive model in India across major political persuasions, reflected in the development models they espouse (Kanwal 2024; Balagopal 2024; Bharatiya Janata Party 2024). Beijing’s success in opening up its economy to foreign and diaspora investment, its central position in global supply chains, and its gradual move up the value chain in both goods and services have inspired similar ambitions in India to become a ‘manufacturing hub’, a ‘major player’, or a ‘global leader’ in various sectors. The red carpet rolled out for big foreign investors like Foxconn (Krishnan 2023b) or Elon Musk (Hindustan Times 2024), for example, reflects the effort to replicate developments in China, as does the increased competition among Indian states to attract such investments and brands. There are different explanations for this fascination with China on both sides of the aisle. For the left, China represents a ‘socialist’ alternative under the leadership of a communist party, and for the right, it exemplifies the achievement of high-scale development through discipline and suppression of dissent. In fact, the Chinese Party-state’s support for large public and private enterprises, as well as its massive infrastructure expansion projects over the years, is echoed in the Bharatiya Janata Party’s manifesto for the 2024 general elections. This is evident from its emphasis on expanding and upgrading transport and digital infrastructure, ensuring energy security, and developing industrial cities along key corridors to promote balanced regional development (Krishnan and Jacob 2024).

The Economic Survey of 2023–24, presented ahead of India’s Union Budget—the first after the new government assumed office in June 2024—further illustrates this benchmarking and provides the clearest indication of intertwined economic relationship between India and China. Beijing’s presence in the Economic Survey may be viewed through two frames: first, as a benchmark or reference point to underline India’s economic reform initiatives; and second, as a source of dependence in trade and investment.[ii] The first frame appears at the very outset, in the preface, meant to guide India’s path ahead:

The global backdrop for India’s march towards Viksit Bharat in 2047 could not be more different from what it was during the rise of China between 1980 and 2015. Then, globalisation was at the cusp of its long expansion. Geopolitics was largely calm with the end of the Cold War, and Western powers welcomed and even encouraged the rise of China and its integration into the world economy’ (Department of Economic Affairs 2024).

This reference point is reinforced in Chapter 5, where China is described as ‘a nation of comparable size and population and antiquity of civilization as India’ that has ‘grown to become a major global economic and political power in less than a generation’ (p. 155). However, an addendum to the Survey adds that China faced fewer challenges during its rise compared to the gamut of issues that shaped ‘India’s growth, prosperity and superpower aspirations for the next quarter century’ (p. 156). These include the Russia–Ukraine and Israel–Hamas conflicts, frequent attacks on the Red Sea trading route, and a growing trend of protectionism and deglobalisation.[iii]

The agricultural reforms undertaken in China between 1978 and 1984 in China are frequently cited references for emulation in India. Known as the ‘household responsibility system’ (lianchandaohu), these reforms encouraged peasants with small landholdings to diversify their produce and promote allied sectors such as animal husbandry, dairying, and fisheries, thereby raising real incomes. Beyond the Survey, various Indian state governments have drawn on the China model and adapted it to their own development plans. Examples include the construction of an industrial housing complex by Tamil Nadu for over 18,000 women workers at a Foxconn plant (Moneycontrol 2024), and the Kerala government’s exploration of Special Development Zones around the new Vizhinjam Port (Balagopal 2024).[iv] Prime Minister Narendra Modi’s ideas also have implicitly benchmarked Chinese experiences, as evident in his Independence Day speeches in 2014 and 2025. These include the overhaul of the Planning Commission and calls for building an indigenous social media and digital infrastructure in India (Modi 2014; 2025).

Persisting Trade Imbalance: Enduring Dependence on China

The political rapproachment in India–China relations after the 1962 war formally took shape with the visit of then Indian Prime Minister Rajiv Gandhi to Beijing in 1988 and his meeting with Deng Xiaoping. The visit also led to the setting up of a Joint Group on Economic Relations, Science and Technology, led by the commerce ministers of both sides (Embassy of India, Beijing 2025). However, it was the Political Parameters Agreement signed during Chinese Premier Wen Jiabao’s visit to Delhi in 2005 that laid the foundation for managing the economic relationship between the two countries (Ministry of External Affairs 2005). Article 1 of the Agreement states that ‘differences on the boundary question should not be allowed to affect the overall development of bilateral relations’.[v]

In 2005–06, China became India’s second largest trading partner, accounting for 9.4 per cent of India’s global trade (when combined with Hong Kong). Bilateral trade stood at US$17 billion, with a surplus of US$4.1 billion in China’s favour. India became a member of the World Trade Organization (WTO) in 1995 (having been a member of its predecessor, the General Agreement on Tariffs and Trade, since 1949) while China joined in 2001. During this period, India was also strengthening its ‘Look East’ policy, concluding bilateral trade agreements with Thailand and Singapore, while continuing negotiations with member countries of the South Asian Association for Regional Cooperation (SAARC) and the Bay of Bengal Initiative for Multi-Sectoral Technical and Economic Cooperation (BIMSTEC). It also set up study groups to boost trade with China, Japan, and South Korea (Pai 2025).

Bilateral trade is the most common and intuitive component of any discussion on India–China economic engagement. It was in 2007–08 that the first signs of imbalance in trade flows were detected, when India’s trade deficit reached US$16.2 billon (Ministry of Commerce and Industry 2010). Since then, trade has continued to expand—despite fluctuations in the political and foreign policy relationship—with China consistently ranking as either India’s largest or second-largest trading partner each year. However, alongside the continued expansion of trade, the widening trade deficit has remained a persistent concern. Imports from China have easily and vastly outpaced exports. Table 1 shows the figures of bilateral trade between the two countries in the last decade: in Financial Year (FY) 2024–25, India’s total trade with China stood at US$127.7 billion, of which imports constituted US$113.4 billion. Thus, India’s trade deficit with China reached US$99.1 billion, accounting for 35 per cent of India’s total trade deficit (Taneja et al 2025) and marking the largest deficit India holds with any single country.

Table 1

India’s Trade with the People’s Republic of China (in US$ billion)

|

Financial Year |

Exports |

Imports |

Total |

Trade Balance |

|

2014–15 |

11.9 |

60.4 |

72.3 |

-48.5 |

|

2015–16 |

9 |

61.7 |

70.7 |

-52.7 |

|

2016–17 |

10.2 |

61.3 |

71.5 |

-51.1 |

|

2017–18 |

13.3 |

76.4 |

89.7 |

-63.1 |

|

2018–19 |

16.8 |

70.3 |

87.1 |

-53.5 |

|

2019–20 |

16.6 |

65.3 |

81.9 |

-48.7 |

|

2020–21 |

21.2 |

65.2 |

86.4 |

-44 |

|

2021–22 |

21.3 |

94.6 |

115.9 |

-73.3 |

|

2022–23 |

15.3 |

98.5 |

113.8 |

-83.2 |

|

2023–24 |

16.7 |

101.7 |

118.4 |

-85 |

|

2024–25 |

14.3 |

113.4 |

127.7 |

-99.1 |

Source: Export Import Data Bank (various years). Ministry of Commerce and Industry, Government of India.

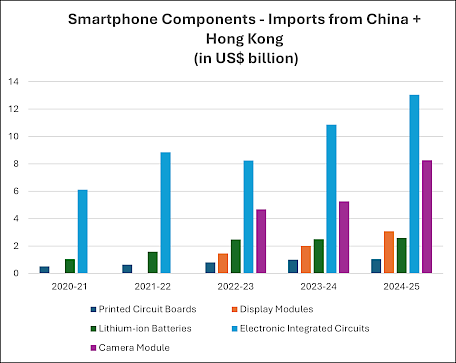

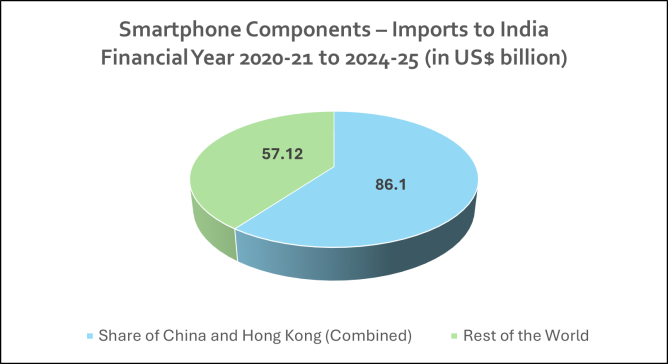

Exports to China include iron ore, shrimp and other marine products, castor oil, spices, organic chemicals, and electrical machinery. Imports from China consist largely of machinery, electronic goods, personal computers, integrated circuits, telephonic/telegraphic equipment parts, components for solar power and other renewable energy systems, plastics, pharmaceutical intermediaries, auto components, lithium-ion batteries, fertilisers, and organic chemicals. While the import basket heavily outweighs exports, it is notable that the bulk of imports from China comprises components, raw materials, and intermediate goods. Chinese suppliers have long provided convenience and ease of doing business for Indian industry. Therefore, any disruption in these supply lines can considerably hinder operations, forcing Indian industry to seek less convenient options. A major share of these components and intermediate goods falls within the electronics sector, classified under HS Code 85 in the global trade and shipments ecosystem. Figure 1 and Figure 2 below present a subset of this sector—smartphone components—imported from China and Hong Kong between FY 2020–21 and FY 2024–25. Figure 1 shows that all five major components critical to smartphone production are sourced from mainland China and Hong Kong.

[i] Marx’s argument was essentially that relations of production as a whole constitute the economic structure of society, which forms the real foundation upon which arises a legal and political superstructure, and to which correspond definite forms of social consciousness. For more, see: Marx, Karl. 1859. A Contribution to the Critique of Political Economy, Preface. Progress Publishers, 1977. https://www.marxists.org/archive/marx/works/1859/critique-pol-economy/preface.htm

[ii] Interestingly, China/Chinese had 156 mentions in the Survey, making it the most mentioned country, while the United States came next, with 107 mentions. This clearly reflects China’s heft in India’s economic calculus.

[iii] This perception in the Indian Economic Survey of China’s challenges is misplaced. China’s transition to a Party-state guided market economy was a protracted process where consensus building within the ruling Communist Party was an uphill challenge. For more, see: Bramall, Chris. 2008. Chinese Economic Development. Routledge; Riskin, Carl. 1987. China’s Political Economy: The Quest for Development Since 1949. Oxford University Press; Weber, Isabella. 2021. How China Escaped Shock Therapy: The Market Economy Debate. Routledge.

[iv] The development of Special Economic Zones around Vizhinjam seems to be inspired primarily by the experience of Shenzhen in the 1970s and 1980s. The Kerala Government’s proposal envisages public–private partnerships and attracting investment from non-resident Keralites, among others, which is similar to the path traversed by China in its early years of economic reform. For more on the emergence and development of Shenzhen, see: Zhou Taomu. 2021. ‘Leveraging Liminality: The Border Town of Bao'an (Shenzhen) and the Origins of China's Reform and Opening’. The Journal of Asian Studies 80(2): 337–361 https://doi.org/10.1017/S0021911821000012

[v] In fact, the Chinese continued to stick to this position, even during the developments in Eastern Ladakh in 2020 and after the disengagement of troops in 2024. The push to compartmentalise different strands of the relationship was repeated by the Chinese Ambassador to Inda, Xu Feihong, in a media interaction in November 2025. See https://www.youtube.com/watch?v=WPpH0gUFrT8.

Figure 1

Smartphone Components imported from China and Hong Kong

between FY 2020–21 and 2024–25

Source: Created by the Author from figures in EXIM Data Bank. Ministry of Commerce and Industry. Government of India, 2025.

Figure 2

Volume of Import of Smartphone Components to India (FY 2021-2024-25)

Source: Created by the Author from figures in EXIM Data Bank, Ministry of Commerce and Industry, Government of India, 2025.

When extended to the entire electronics sector, the dependence becomes even more pronounced. Of the total US$34.4 billion imports in FY 2023–24, a combined US$18 billion came from China and Hong Kong; by comparison, in FY 2019–20, out of the total imports of US$16 billion, China and Hong Kong had a combined share of US$10 billion (Department of Commerce 2024, as cited in Barik 2024). Even as India has emerged as an electronics assembly hub over the past decade, the industry remains heavily dependent on China for sourcing the core components of the sophisticated devices.

Non-tariff Measures (NTM) headline the disproportionately low Indian exports to China. NTMs are classified as policy measures—other than customs tariffs—that can potentially have an economic effect on international trade in goods by changing quantities traded, prices, or both (United National Conference on Trade and Development 2019). Most NTMs fall in the Sanitary or Phytosanitary (SPS) or Technical Barriers to Trade (TBT) categories, which impose technical regulations that set product characteristics or production processes. In addition, there are non-technical measures, such as licenses and quotas, price affecting measures, as well as financial or exchange rate regulations. At a basic level, NTMs are regulatory measures imposed by the home, partner or sometimes transit countries that have direct and/or indirect effects on trade costs (United National Conference on Trade and Development 2013). The main non-tariff barriers faced by Indian exporters to China include the following (Press Information Bureau 2019; Tantri et. al 2021; Mishra 2023; Taneja et. al 2025).

- Complex regulations and non-transparent procedures: These include multiple regulatory requirements for safety, quality, certification, and testing, which are often characterised by opaqueness, changing rules, and limited availability of information in English. Additionally, domestic market protections for Chinese producers make it harder for Indian exporters to compete, even if they meet technical requirements.

- Technical Barriers to Trade: These refer to stringent standards in sectors such as food, agriculture, dairy, meat, fish, and processed food, often resulting in repeated rejections of consignments or lengthy delays.

- High compliance and transaction costs: These are costs arising out of inspection, certification, conformity assessments, documentation, and re-testing requirements (such as restrictions on third-party laboratories), and language or documentation barriers.

- Lack of effective redressal or appeal mechanisms: Once a consignment is rejected on quality or safety grounds, exporters have limited avenues for recourse.

Over the years, NTMs have become barriers that undermine the possibility of a level playing field in the economic engagement between India and China. This issue has consistently figured in bilateral negotiations, leadership dialogues, and diplomatic visits. Despite the existence of institutional mechanisms for economic dialogue, unequal market access for Indian companies in China’s domestic markets remains unresolved. While China has repeatedly pushed India to normalise relations and prevent boundary disputes from overwhelming economic ties, it has remained non-committal on reducing non-tariff barriers.

Chinese Investments in India

Even as bilateral trade between the two countries has increased, this has not been matched by growth in bilateral investment, despite both emerging as major investment destinations for the rest of the world. According to China’s Ministry of Commerce, Chinese investment in India stood at US$60.37 million in 2023, with cumulative investments of US$3.2 billion between 2015 and 2023 (Embassy of India, Beijing 2025). According to data from India’s Department for Promotion of Industry and Internal Trade, the Chinese Foreign Direct Investment equity flows into India between January 2000 and March 2025 totalled US$2.5 billion (rising to US$7.3 billion when combined with Hong Kong) (2025).

In 2014, during Xi Jinping’s maiden visit to India and the Chinese government’s meetings with the newly elected National Democratic Alliance government led by the Bharatiya Janata Party, there was palpable anticipation of Chinese investment, with media reports even speculating inflows of up to US$100 billion over five years (Pandey 2014). However, even the US$20 billion worth of Memoranda of Understanding (MoUs) signed did not materialise (Embassy of India, Beijing 18 September). Two proposed industrial parks—in Gujarat and Maharashtra—planned in partnership with China Development Bank Corporation and Beiqi Foton Motor Company Limited, respectively, did not make any real progress. In 2017, two more MoUs were signed for Chinese investment in Haryana by the state’s Industrial Development Corporation for projects including an integrated entertainment park-cum-industrial township involving Dalian Wanda group and an industrial park in partnership with China Fortune Land Development (Ministry of Commerce and Industry 2017). Yet, none of these projects have moved beyond the initial announcements.

In the case of the Beiqi Foton Motor Company Limited project in Maharashtra, which had been on the horizon since 2011, the state government had completed the formalities of land acquisition. However, the project faced several delays and eventually stalled due to a clash with native cultural practices and the company’s difficulties in navigating complex local political and regulatory dynamics (Chauhan 2015; Bradsher 2015). Moreover, military tensions in Doklam in the summer of 2017 and in other areas along the LAC, also changed the political conditions, and put paid to any chances of the MoUs translating to infrastructure on the ground. Another concern has been the complete opacity surrounding these MoUs and the lack of proper communication from the government on their status. Much like in other facets of the relationship, lack of accountability also seeps into the realm of economic engagement.

In a written reply to a question raised in the Lok Sabha in 2022, Rao Inderjit Singh, then Minister of State for Corporate Affairs, stated that 174 Chinese companies were registered in India as foreign companies with businesses in the country after due approvals from the Reserve Bank of India (RBI) under the Foreign Exchange Management Act (2022). Additionally, there were 2,488 FDI inflows from Chinese companies, according to the information provided by the RBI (Thakur 2021). Notwithstanding this data, the exact number of Chinese companies operating in India has been difficult to ascertain as FDI is also routed through third countries (Krishnan 2020).

Since 2010, Chinese companies have expanded beyond infrastructure, power, energy, and telecommunications into sectors such as consumer electronics, factory machinery, and digital technology. Up to March 2020, Chinese technology investors had invested US$4 million in Indian start-ups (Bhandari, Fernandes and Agarwal 2020). The most salient investments have been in the smartphone, automobile and power sectors (Baijiahao 2022).

Structural factors within China, including overcapacity in manufacturing, domestic market saturation, and rising competition have forced companies to look outwards (Yicai 2015). India’s large population, rising consumption, younger workforce, and rising demand make it an attractive destination for long-term growth and scale. Its growing consumer base has also attracted these companies, which see India’s financial system and active securities market as better suited to facilitate their operations (Yicai 2015; China Council for Promotion of International Trade 2022). Moreover, Chinese firms see India as a base from which to manufacture and export to markets like the USA and the European Union amid global supply chain diversification (Majumder 2024). For many Chinese firms, India is seen as more economically relatable than the ‘foreign West’, with lower barriers to expansion—especially in sectors such as manufacturing and infrastructure—thus allowing them to leverage existing strengths (Wang 2022).

There have been three phases in the evolution of Chinese corporate presence in India (Zhufan Research Institute 2019, as cited in Ghosal Singh 2024):

- Before 2010: Primarily focused on infrastructure sectors including power, telecommunications, roads and bridges, rail transit and energy;

- 2010–2016: Expansion into competitive sectors such as consumer electronics, high-end services, healthcare and pharmaceuticals, factory machinery, and building materials;

- Post-2016: Large-scale investments in manufacturing and internet-based sectors.

China’s ‘Going Out’ strategy (zouchuqu zhanlüe), adopted in 2000 and on whose shoulders the Belt and Road Initiative (BRI) was initiated since 2013, has extended the reach of Chinese capital beyond the country’s territorial boundaries. Both state-owned enterprises and private companies have been encouraged by the Party-state to expand their operations internationally while maintain their Chinese identity. According to China’s State Administration of Market Regulation, as of 2024, there are over 55 million private companies in the country (Xinhua 2025c). The private sector accounts for over 50 per cent of China’s tax revenue, over 60 per cent of GDP, more than 70 per cent of technological innovation, over 80 per cent of urban employment, and more than 90 per cent of the total number of enterprises (Qiushi 2023). In comparison, India’s private sector accounts for 36 per cent of tax revenue, 91 per cent of GDP, 36 per cent of technological innovation, 11 per cent of employment, and over 95 per cent of the total number of registered enterprises (Department of Science and Technology 2023; Waghmare 2024; Ministry of Statistics and Programme Implementation 2024; Dhoot 2024; Statista 2025).

In mid-February 2025, CPC General Secretary Xi Jinping met the country’s private business leaders at a symposium in Beijing (Xinhua 2025b, where emphasized the importance[i] of the companies to embrace patriotism (Xinhua 2025a). This vote of confidence from the Chinese leadership served as an acknowledgement of the rising importance of China’s private capital in driving not only domestic development but also its global economic ambitions. An apt illustration is the unveiling of two open-source models by Chinese Artificial Intelligence company, DeepSeek, in the beginning of 2025, challenging the dominance of American rivals such as OpenAI, Meta and Google.

Chinese outbound investment is now increasingly driven by the expansion of globally ambitious private companies with a growing focus on emerging markets rather than high-income economies (Hanemann et. al 2024). These companies are involved in diverse internationalisation efforts across value chain segments, such as establishing local manufacturing, sales, and service operations. According to China’s General Administration of Customs, in 2024, Chinese private enterprises accounted for foreign trade transactions worth 24.33 trillion yuan (approximately US$3.4 trillion) (Xinhua 2025).

Chinese private companies, with their sleek and sophisticated products, have been able to connect with global consumers and serve as pivotal entities in building an ‘industrial diplomacy’—to borrow a phrase from sociologist Kyle Chan—reshaping global production networks and centring them around Beijing (2025). This is visible in strategic sectors, such as electric vehicles, consumer electronics and digital gadgets, lithium batteries, and solar panels (Pierce 2017; International Energy Agency 2022; Wu 2024; Kaku 2024; Ren and Xue 2025). Chinese private companies form vital nodes in global supply chains in these industries, and their inextricability is used by Beijing for competitive advantage (Li and Cheng 2024). Through these companies, China has remained attentive to building backward and forward industrial linkages—through the manufacturing of components and specialised machinery, along with the development of skilled personnel with technical know-how—and holistically dominated the wider ecosystem while also guarding against the sharing of technology.

From 2014 to 2018, India ranked 31st among destinations for Chinese outward investment (Pranav 2019). A survey—the first of its kind—conducted by the Industrial and Commercial Bank of China’s Mumbai branch revealed that 431 Chinese companies entered the Indian market in 2014 (China Council for Promotion of International Trade 2017, as cited in Ghoshal 2024). Another survey in 2019 by consulting firm Zhufan Research Institute found that the number of Chinese companies in India tripled between 2010 and 2016 compared to the pre-2010 period, and doubled again between 2016 and 2019 (Zhudao 2019, as cited in Ghoshal 2024).

A case study illustrates the nature of Chinese corporate presence in India, focusing on Shanghai Zhenhua Heavy Engineering Company Limited, a state-owned enterprise and the leading supplier of equipment for concessionaires/authorities of ports across the globe, and its rise to dominance in the sector.

Port Infrastructure: Shanghai Zhenhua Heavy Engineering Company Limited

On 2 May 2025, Prime Minister Narendra Modi commissioned the Vizhinjam International Seaport Limited (VISL), the country’s first fully automated deep water transshipment port, built at a cost of ₹8,867 crore (US$1.06 billion). The port is fully owned by the Kerala state government, with some support from the central government, and the multi-purpose project was executed by Adani Ports and Special Economic Zones Limited. A notable aspect of the project is that all 32 fully automated cranes used in port operations were provided by Shanghai Zhenhua Heavy Engineering Company Limited (ZPMC) (2024). These include eight rail mounted quay (ship-to-shore) cranes used for loading and unloading containers between ships and docks, and 24 rail-mounted gantry (yard) cranes. Founded in 1992, ZPMC is a wholly owned subsidiary of China Communications Construction Company, a state-owned enterprise. The company specialises in designing, manufacturing, shipping, erecting and commissioning new port machinery products. Among its vast range of products, the most critical ones are different types of cranes. In addition to these, ZPMC has supplied a comprehensive portfolio of terminal-related operating sub-systems to Vizhinjam, including software for container management, refrigeration systems, and guaranteed spare parts and servicing support.

The company claims a presence in 106 countries, and, as showcased through its active social media handle, its machinery and equipment have been utilised in numerous newly built ports across the globe. ZPMC holds a 70 per cent market share in quay/ship-to-share cranes, and has also ventured into infrastructural initiatives beyond ports (Gonzales 2011). This expansion has occurred despite allegations from competitors that the company replicated their designs (Reiterman 2002)—claims later acknowledged by its founder, Guan Tongxian (Fu 2018). The launch of BRI significantly raised the profile of ZPMC, which had faced seen operational losses on account of a global financial crisis in the intervening period (Plötner and Wang 2013). As infrastructure development became the kernel of BRI, ZPMC’s stocks rose as the company claimed the presence of its equipment in 270 ports worldwide and a dominant market share of 80 per cent (McGregor 2023).

One of ZPMC’s key advantages lies in its large manufacturing facility located on Changxing Island near Shanghai, which is dedicated to manufacturing container handling equipment, enabling the company to minimise building, assembling and inventory costs (Federal Highway Administration 2016). Fully assembled cranes at the facility are then delivered to client ports using the company’s own dedicated shipping fleet (Federal Highway Administration 2016). ZPMC also offers lifetime servicing and spare parts for the machinery, thus extending its relationship with port authorities for significantly longer durations. The company exemplifies China’s dominance in global port infrastructure, as competing non-Chinese companies lack the deep pockets to pose a challenge, as dependable and attractive alternatives for global developers and clients (Council on Foreign Relations 2024).

In 2024, a US Congressional probe revealed that communication equipment installed on more than 200 ZPMC cranes in American ports had not been documented in contracts between the company and the ports, raising concerns about surveillance and/or sabotage (Volz 2024). While the company denied these accusations, the episode highlighted vulnerabilities in critical infrastructure and raised broader questions about national security. Interestingly, India had already placed restrictions on ZPMC and its equipment at the Jawaharlal Nehru Port in Mumbai in 2013 (Manoj 2013). This was in line with the central government’s policy, adopted in 1997, barring Chinese companies, or groups with connections to China, from participating in Indian port projects.

This move, which also extended to ports built by India outside its territorial jurisdiction (Manoj 2020), raised apprehensions among port concessionaires and developers (Manoj 2014) about delays in meeting their targets, prompting the Ministry of Shipping to urge security agencies to reconsider their stance (Manoj 2014). In fact, in February 2024, questions were raised in the Rajya Sabha on the use of more than 250 ZPMC cranes across Indian ports as of end-2020, which was admitted by the government, citing adherence to extant rules and guidelines by all operators (Rajya Sabha 2024).

In April 2020, the central government introduced restrictions on public procurement from countries sharing a land border with India on grounds of national security. These rules applied to various entities, including public–private partnership projects receiving financial support from the government. As these provisions extended to the Vizhinjam project, the argument put forth for the continued procurement of cranes was that Adani Ports had placed its orders with ZPMC in 2018, and therefore, the restrictions did not carry retrospective effect (Kumar and Wani 2024). Further, a positive spin was given to the narrative with the claim that the procurement contributed ₹334 crore (US$40.24) to the exchequer in the form of Goods and Services Tax (Asianet News 2025). This reflects the contradictions between policy positions and their implementation. Looking ahead, the number of cranes is set to increase from the current 32 to 100 in the second phase of the port’s development, scheduled to commence at the end of January 2026 (The Hindu 2026). As the current supplier, ZPMC is poised to provide the required equipment and further deepen its existing relationship with the port.

Difficulties in Discounting China from the Policy Calculus

The Economic Survey of 2023–24, presented ahead of the first Union Budget of the newly elected NDA government in 2024, highlights the unavoidability of Chinese trade and investment for India. Chapters 4 and 5—on the External Sector and Medium-Term Outlook—outline a narrative of dependence on China and argue for closer relations to fuel India’s economic and manufacturing ambitions. The Survey highlights China’s dominance in global supply chains across product categories, noting, for example, ‘China’s near-dominance over the production and processing of critical and rare earth minerals’ (p. 161). This dependence poses concerns for India’s renewable energy programme, given its heavy reliance on Chinese imports of raw materials (Tagotra 2023; Janardhanan 2021). The Survey provides an official acknowledgment from the Indian government—or at least within sections of it—of the dilemma between national security considerations and economic necessity in managing relations with China, given its currently inevitable—and irreplaceable—role in India’s manufacturing ambitions and economic growth.

While the Survey recognises the utility of the China Plus One strategy,[ii] it cautions against overreliance on this approach, from the perspective of deepening India’s integration into global value chains. It underlines the need to look at the ‘successes and strategies of East Asian economies’, whose track record is based on two policies: ‘reducing trade costs and facilitating foreign investments’ (p. 143–144). Citing examples such as Vietnam, Taiwan and South Korea as well as Mexico, the Survey points out that while these countries were ‘direct beneficiaries of the US’ trade diversion from China’, they ‘also displayed a concomitant increase in Chinese FDI’, reinforcing that the ‘world cannot completely look past China’ (Gourinchas 2024, as cited in Department of Economic Affairs 2024: 144). In this context, the Survey recommends prioritising Chinese FDI over trade, especially given New Delhi’s continuing trade deficit with Beijing. Its reasoning is that ‘as the US and Europe shift their immediate sourcing away from China, it is more effective to have Chinese companies invest in India, and then export the products to these markets rather than importing from China, adding minimal value, and then re-exporting them’ (p. 144). This strategy also serves to mitigate the risk of economic coercion—whereby China could restrict access to critical inputs for political leverage—by embedding production within India rather than remaining dependent on external supply chains (Boullenois and Jordan 2024).

The Survey emphasises India’s need to find the right balance between imports of goods and inflows of capital (FDI) from China. It draws on the experience of countries such as Brazil and Turkey in the electric vehicle (EV) sector, where governments have simultaneously raised barriers on Chinese EV imports while adopting measures to attract Chinese FDI in the sector.[iii]

The Survey argues that it ‘may not be the most prudent approach to think that India can take up the slack from China vacating certain spaces in manufacturing’, since it remains doubtful whether China has vacated those spaces in the first place (p. 161). Noting that China ‘imports very few low-tech goods’ as part of its ‘deliberate policy interventions, which have intensified in recent years’ (p. 162), it suggests that India should adopt a similar pathway in the medium to long-term.

Import restrictions on Chinese goods have expanded across emerging market and developing economies, including India, amid threats of industrial overcapacity in China overwhelming their domestic manufacturing sectors. However, meeting this competition must go hand in hand with ‘boosting domestic manufacturing capabilities, sometimes with the collaboration of Chinese investment and technology’—in sum, to boost Indian manufacturing and plug India into the global supply chain, it is inevitable that India plugs itself into Chinese supply chains (p. 163). While underlining the centrality of Micro, Small and Medium Enterprises (MSMEs) to India’s future growth—‘contributing approximately 30 per cent of the country’s GDP, 45 per cent of its manufacturing output, and providing employment to 11 crore Indians (Invest India 2023)—the Survey stresses the need for ‘striking the right balance between the trilemma of trade with China, investment by China, and India’s territorial and non-territorial integrity and security’ (p. 167).[iv]

This push for a more flexible and pragmatic set of economic policies with respect to China is not entirely new; it has been voiced even after tough measures such as Press Note 3[v] and later developments in Eastern Ladakh. Economists have repeatedly pointed to India’s dependance on China for components, even to the extent of tempering high-decibel campaigns such as the ‘Aatmanirbhar Bharat Abhiyan’, and narratives of Delhi replacing Beijing as the manufacturing powerhouse (Dhar and Rao 2020; Subramanian and Felman 2022; Felman and Subramanian 2024; Mody 2024; Rajan and Lamba 2024). Industry groups and India Inc. have consistently called for concessions and reconciliation in India’s economic engagement with China, warning that escalating tensions could have a debilitating effect on production and employment. Production losses in the electronics sector, estimated at US$15 billion, are a case in point (Mallick 2024). The Confederation of Indian Industry, while asking for fiscal support from the government to increase domestic value addition in the electronics industry, has also sought a ‘non-restrictive approach towards investments, component imports, technology transfer between partners’ and the enabling of ‘non-restrictive movement of skilled manpower from competing economies’, insisting on a review of Press Note 3 (2024: 4).

Similarly, one of the most important local interest groups, the India Cellular and Electronics Association has consistently lobbied with the government for its network of manufacturers affected by the restrictive environment, seeking the ease of visa restrictions on Chinese technicians and reduction in import tariffs (Mallick and Rathee 2023; India Cellular and Electronics Association 2024). Notably, the push by the Ministry of Electronics and Information Technology and the Ministry of Commerce and Industry to ease visa norms for Chinese technicians within days of the new government taking office illustrates the complexity of economic relations, where a blanket negative position is difficult to sustain (Mishra and Barik 2024).

The Economic Survey, while providing a medium-term outlook and growth vision for India, undergirds the importance of skill development in education, right from the school level, to ‘harness the demographic dividend’ and ‘be prepared for the needs of the industry’ (p. 172). The creation of a young, quality workforce fostered by innovation and entrepreneurship, with employability as a key criterion, is central to India’s economic aspirations. As it is, employment generation is also a political question, going by the results of the 2024 general elections and the subsequent announcements made by the finance minister in the union budget. Interestingly, the Chinese Party-state is grappling with similar challenges as it pursues high-quality development, prioritising talent, education and innovation, especially with the demographic challenge of an ageing society (Communist Party of China 2024).

Announcements in the Union Budget 2024–25—including cuts in custom duties on mobile phones and components by 15 per cent, and increased allocations under the Production Linked Incentive (PLI) scheme for large-scale electronics manufacturing through the allocation of ₹6,125 crore—indicate some concessions. Chinese companies have mostly stayed away from PLI though they are now doing it through JVs with Indian entities as part of the electronics components manufacturing scheme (Khan 2025; Chennamkulath 2025).

Press Note 3 in 2020 and Its Amendments: Economic Necessities and Global Realities after Six Years

In April 2020, during the early days of the COVID-19 pandemic, the Indian government revised its FDI policy by making it mandatory for countries sharing a land border with India to route their investments only through the government—an implicit reference to China (Department for Promotion of Industry and Internal Trade 2020). Known by the shorthand Press Note 3, this tightening of rules was meant to prevent opportunistic takeovers of Indian entities by Chinese firms (Unnikrishnan 2020). From then on, the government’s position became more stringent, which had a cascading effect on Chinese investments: existing investments were subject to increased scrutiny and restrictions, including punitive actions (Press Trust of India, 2023; Indian Express, 2023; Kalra, 2022) while prospective investors grew increasingly cautious, often reconsidering their plans to enter the Indian market within this unfavourable ecosystem.

On 10 March 2026, the union cabinet amended Press Note 3 to ease curbs placed on investments from countries that shared land borders with India, thus revising the restrictions in place since 2020 (Press Information Bureau 2026b). This amendment introduced a 60-day window for the processing of investment proposals in specified sectors, such as capital goods manufacturing, electronic capital goods, electronic components, and polysilicon and ingot-wafers (key inputs for solar cells), to encourage more Joint Ventures (JVs) between Indian and Chinese entities (Pai 2026). Over 2025, the central government has approved JV proposals involving Indian and Chinese electronics manufacturing companies like Dixon and Longcheer.

While investments of up to 10 per cent in these priority sectors may qualify for automatic approval, the revised norms stipulate that the majority shareholding and control of the investee entity must remain with resident Indian citizens and/or resident Indian entities owned and controlled by them at all times. Additionally, a Committee of Secretaries under the Cabinet Secretary has been given powers to revise the list of eligible sectors. By amending Press Note 3, the central government seeks to enable more investment flows from mainland China. The decision comes after growing calls from India Inc., stakeholders in the manufacturing and allied sectors, as well as policymakers, to facilitate ease of doing business for Chinese entities. This is being seen as critical for India’s industrial and economic growth and transformation, especially in the wake of the current global economic turbulence induced by US tariff policies. The prolonged conflict in the Middle East further accentuates the uncertainties in the global economic landscape.

The easing of curbs is consistent with the Indian government’s incremental approach toward economic engagement with China following the military disengagement process in Eastern Ladakh in 2024, which further led to Prime Minister Narendra Modi’s visit to China for the SCO Summit in Tianjin in August 2025. New Delhi has since adopted an approach of graded reopening based on mutual reciprocity by Beijing—although such reciprocity has not always been forthcoming (Magazine 2026). Reports in early 2026 suggested that the Ministry of Finance was planning to remove curbs on Chinese firms bidding for government contracts (Ohri and Singh 2026). This would potentially exempt Chinese firms from stringent registration procedures and political security clearances. Similarly, a draft cabinet note circulated to relevant ministries for comments proposes relaxing rules governing equity partnership between Chinese and Indian firms in the electronics and consumer durables sector (Roy 2025). If approved, Indian firms receiving up to 49 per cent investment will no longer be subject to extensive scrutiny. Deep dependence on Chinese components, combined with the complex interdependencies of global supply chains, limits the effectiveness of economic nationalism as a standalone strategy. In this context, rigid restrictions risk undermining flagship initiatives such as ‘Make in India’ which rely on integration into global production networks.

Achieving comprehensive domestic manufacturing—from components to finished products—along with a robust supplier network, requires the development of ancillary industries, clusters for technological knowledge-sharing, uninterrupted power and water supply, and better working and living conditions for India’s workforce. India possesses none of these at scale at the moment. Therefore, there is a need for some compromises as well as greater adherence to federalism in crafting sound policies for India to gain an advantage over China (Jacob 2024). If anything, investment from China may be viewed as a source of foreign policy leverage: the greater the volume of investment, the greater the transfer of risks onto Chinese firms, which in turn remain tied to India’s policy regime (Aiyar 2020).

2020 Eastern Ladakh Transgression and After: The State of Play

The 2020 incursions by the Chinese PLA in Eastern Ladakh and the deadly violence in Galwan Valley had an effect on economic engagements. For the first time, a standoff between the armed forces of the two countries in the high Himalayas had a serious impact on India’s business ecosystem. In the early days after the military standoff—which coincided with the COVID-19 pandemic—India adopted a range of measures, including scaling back promotional activities, toning down high-pitched celebrity advertisements, and amplifying the ‘Make in India’ narrative to highlight its commitment to advancing the country’s manufacturing ambitions (Bhushan, Mukherjee and Sengupta 2020).

Simultaneously, the Indian government tightened the screws on Chinese capital, initiating punitive action on suspicion of tax evasion, money laundering, and illegal foreign remittances (Press Trust of India 2023; Indian Express 2023; Kalra 2022). Along with this increased scrutiny, the government took measures to ‘Indianise’ operations and management in a range of fields and ensure strict adherence to legal and tax-related compliances—including the induction of Indian equity partners in local operations, the appointment of Indian executives to leadership roles, involving Indian contract manufacturers, expanding exports from India, and hiring only local distributors (Mukherjee, Rathee and Chakravarty 2023).

Chinese companies have been able to survive this turbulent phase in India–China relations because of their adaptability. Despite the headwinds emanating from the turbulence in bilateral relations, the steady sales figures of Chinese brands suggest continued consumer confidence. Handset shipments from production facilities in India to Southeast Asia and the Middle East have begun as part of the ambitious ‘Make in India’ initiative, even as the government has pushed for a higher export share from Chinese companies (Business Standard 2023). Further, after dominating other markets, new Chinese smartphone players continue to view India as their next destination (Singh 2024). Chinese companies are prepared for the long haul, seeing the promise and potential in the sheer size of the Indian market. Their future investment and production strategies have been adjusted to align with the Indian government’s vision of transforming the country into a global manufacturing and export hub (VIVO India 2024).

While India is positioning itself as an alternative manufacturing base, it is also grappling with limited domestic capacity. In August 2024, reports emerged that the US Customs and Border Protection Agency (CBP) had detained nearly US$43 billion worth of electronics shipments—specifically, solar panels—from India since October 2023. The CBP’s actions were in line with the Uyghur Forced Labor Prevention Act (UFLPA), enacted under the Biden administration in December 2021 to prohibit the importation of goods manufactured wholly or in part with forced labour in the People's Republic of China, especially the Xinjiang Uyghur Autonomous Region (XUAR). In this case, CBP worked on the assumption that the polycrystalline silicon—a key input in solar photovoltaic (PV) modules and semiconductors—had come from XUAR. The US’ increased scrutiny of Chinese companies over the last few years—under the UFLPA and otherwise—has been seen as an opportunity by Indian policymakers and industry—including the solar industry—to pitch India as a viable alternative to China. The Ministry of New and Renewable Energy, in response to a question in the Rajya Sabha, claimed that India had achieved self-sufficiency in the production of solar modules, with the export of panels worth US$1.03 billion in 2022–23. However, in the same response, the ministry also admitted that the country was yet to reach substantial capacity in the production of solar cells.

The CBP’s actions reveal the extent of enforcement of the UFLPA, where even components within final products are subjected to scrutiny. This development further underscores how Chinese companies, even with their manufacturing capabilities, remain intrinsically linked to India’s manufacturing ambitions. As per data from Delhi-based think-tank, Global Trade Research Initiative, with specific reference to solar panels in FY 2024, imports of assembled PV cells amounted to US$2.9 billion (constituting 65.5 per cent of such imports), while non-assembled cells amounted to US$1.0 billion (accounting for 55.9 per cent of such imports).

In response to pandemic-induced supply chain disruptions, the Indian government accelerated efforts towards achieving self-sufficiency in the renewable energy sector. Extending the PLI scheme introduced for large-sector electronics manufacturing in 2020, a similar scheme for high-efficiency solar PV modules was launched in 2021, to achieve manufacturing capacity at gigawatt scale with an outlay of ₹24,000 crore. It is being implemented in two tranches of ₹4,500 crore and ₹19,500 crore, with 13 companies—many of them indigenous—successfully winning bids. Interestingly, however, a majority of these companies have listed Chinese vendors as suppliers, underscoring the lack of viable alternatives on the one hand, and the tightly intertwined nature of production networks on the other. Similarly, while an outlay of ₹250 crore has been allocated in the Union Budget 2024–25 for the National Programme on Advanced Chemistry Cell Battery Storage under the Ministry of Heavy Industries, there is no specific allocation for any PLI scheme towards solar PV module manufacturing under the Ministry of New and Renewable Energy. The efforts to reduce dependence on China by scaling up and incentivising domestic production might be a good strategy in the long-term. However, in the short-term, it is inevitable for Indian solar companies, constrained by prevailing economic realities and lack of profitable alternate avenues, to ‘plug into China’s supply chain’ (Department of Economic Affairs 2024).

The Indian government has seriously started re-evaluating its strategy to accelerate efforts to build domestic capacity and gradually reduce its dependence on China. The intersection of the shrill rhetoric of boycotting Chinese products with the government’s ‘vocal for local’ campaign has reinforced the emphasis on building self-sufficiency. The introduction of the PLI scheme in 2020—beginning with large-scale electronics manufacturing—to power the ambitious ‘Make in India’ initiative launched in 2014 (Ministry of Electronics and Information Technology 2020; Ministry of Commerce and Industry 2023). At present, the Indian government’s strategy with respect to China seems to rest on two key pillars: encouraging investments from Taiwan, and creating conditions to leverage the ‘China Plus One’ diversification strategy adopted by multinational companies.

Weaponising Supply Chains, Open Coercion: China’s New Muscle Flexing

In mid-January 2025, China reportedly placed travel restrictions on its citizens working as engineers and technicians at Foxconn’s facilities in India (Cheng and Zhou 2025). Those already in India were recalled, and these measures were extended to curbs on the export of critical specialised manufacturing equipment, over which China has a monopoly. While Foxconn reportedly scrambled to bring in Taiwanese workers to fill the gap in manpower, the export restriction on specialised equipment was more crippling. Apple–Foxconn has been critical to India’s ambitions of becoming a global manufacturing power, and therefore, such disruption affects that larger objective.

These zero-sum measures by China reflect an expansion of geopolitical competition with India in the economic domain through regulations on the flow of capital and other factors of production. Fully cognisant of its dominance in advanced machinery and its well-trained workforce within tightly integrated global electronics production networks, China also intends to curb the tacit transfer of knowledge from its technicians to their Indian counterparts on the assembly line (Luk 2025). Combined with the disruptions on specialised equipment supply, this strategy weaponises China’s strategic position in the network of supply chains to slow down production in India while placing itself in an advantageous negotiating position.

The growing trade tensions between China and the West, specifically the United States, along with pandemic-induced disruptions, have led many global corporations to adopt ‘China Plus One’ diversification strategies to future-proof themselves. India has been at the forefront to seek benefits from this move, along with countries like Vietnam and Mexico. Given the scale and evolution of India’s manufacturing sector, along with its potential to replicate China’s manufacturing trajectory, Beijing realises the need to limit the rise of its geopolitical rival and remind global corporations of its own indispensability to the production ecosystem.

Large-scale electronics manufacturing, especially of smartphones, is an important pillar of the Make in India programme. The PLI scheme, first introduced in the electronics industry in 2020, has witnessed increased allocations by the central government— from ₹6,125 crore in Union Budget 2024–25 (US$0.73 billion) to ₹8,885 crore (US$1.02 billion) in Union Budget 2025–26. From FY2022–23 to FY2024–25, Apple’s contract manufacturers in India—Foxconn, Pegatron and Tata Electronics—had cumulatively received close to ₹6,600 crore (US$0.76 billion) of the total disbursed amount of ₹8,700 crore (US$1 billion) (Barik 2025). In addition, Union Budget 2025 has eliminated basic customs duties or import taxes on mobile phone components—such as printed circuit boards, camera modules, connectors, and sensors—as well as on capital goods and machinery used in the manufacturing of lithium-ion batteries for mobile phones. The central government’s priority in championing the electronics industry to project the country’s growing manufacturing capabilities is well visible through these measures.

It is notable that China’s zero-sum action occurred just a few months after the October 2024 patrolling agreement with India that ended a four-year military standoff between both armies in eastern Ladakh. Economic necessity—visible in the Indian dependence on China for components and machinery—is believed to have hastened the negotiation process. This illustrates how India–China relations do not necessarily hinge on a stable boundary, as geopolitical competition between the two sides is bound to become more acute in the future. The fact that restrictions on machinery and equipment have been extended to tunnel boring machines (Sharma 2024) and rare earth minerals (Pandey 2025) exemplifies China’s zero-sum approach to slow down India’s industrial-infrastructural development and hold on to an advantageous negotiating position. While some of these restrictions may have workarounds (Kumar and Kotasthane 2025), they underscore China’s muscle flexing and its negative effects for India’s domestic manufacturing ecosystem. While Indian industry has voiced the need to reduce dependence on China, it has also called for greater inflows of Chinese FDI in key sectors such as electronics (Confederation of Indian Industry 2024) by reconsidering restrictions on investments from countries sharing land boundaries with India.

China has also employed ‘lawfare’—law + warfare[vi]—to exert pressure through multilateral fora like the WTO. In October, it approached the Dispute Settlement Body of the WTO over India’s incentives for its domestic EV sector. Beijing challenged New Delhi’s three PLI schemes, claiming that they were contingent upon the use of domestic over imported goods and discriminate against goods of Chinese origin (World Trade Organization 2025). While two of these schemes, introduced in 2021, affect manufacturers of EV batteries, components, and original equipment, the third—brought into effect from March 2024—slashes import duties on fully built passenger EVs from 110 per cent to 15 per cent for cars priced above US$35,000, and capped at 80,000 units annually (Press Information Bureau 2025b). China’s escalation of the matter is based on two factors. The first is the dominance of Chinese companies in the EV industry and the pressures of domestic overcapacity driving a search for new markets, including India. The second is the development of Indian companies in the sector, which poses a competitive challenge for Chinese firms in the long term. It is worth noting that Indian automobile manufacturers in the EV sector remain dependent on Chinese components, especially magnets (Sasi 2025). China’s stranglehold on rare earth elements (REEs), crucial for the production of magnets, has also forced Indian companies to rethink their production models. They have been forced to import expensive, entirely built motor components from China and Vietnam, and to adopt temporary workarounds by cutting down on certain equipment (Mishra and Barik 2025). On 24 February 2026, the Dispute Settlement Body of the WTO agreed to establish a panel to review India’s measures, with New Delhi expressing concern over China’s actions and receiving support from Washington DC on the issue (2026).

In the short term, India faces limited options and may need to negotiate with China to ease export controls. However, this may also serve as an opportunity to future-proof its manufacturing ecosystem in terms of human resources, components and specialised machinery. It needs to be kept in mind that India is still largely a centre for the final assembly of smartphones. For a well-rounded and holistic manufacturing ecosystem that includes the production of various components, ancillary industries need to be incentivised and scaled up. The National Manufacturing Mission, announced in Union Budget 2025–26 and intended to strengthen small, medium and large industries, is a good step, but will need credible financial muscle that leads to the development of clusters for technological knowledge-sharing.

Skill development programmes must incorporate on-site training for workers—including tacit knowledge sharing on assembly lines—while being complemented by industry-specific specialisation. Encouraging greater private capital will help create a robust network of indigenous contract manufacturers that can serve not only foreign corporations but also domestic Indian brands. India’s transformation into a manufacturing hub, with China as a model, is one of the priority objectives for the Narendra Modi government. Initiatives such as the Make in India campaign and PLI schemes are designed to provide a fillip to this ambition of attaining self-sufficiency. India has also been actively seeking benefits from the China Plus One diversification strategy developed by Western corporations to find alternative production bases and de-risk their businesses, learning from their experience of COVID-related disruptions in China. However, this strategy now faces fresh challenges, particularly after the 50 per cent tariffs imposed by the Trump administration, which took effect on 27 August 2025.

As a geopolitical rival, Beijing is aware of New Delhi’s measures to benefit from the China Plus One diversification strategy, which is also aligned with its own manufacturing ambitions. India’s rise as an industrial power and its pursuit of self-sufficiency is inimical to China’s established position as the ‘workshop of the world’. In response, China has chosen to choke supply lines to Indian industry, forcing the Indian government to seek adaptive responses. During a meeting with Chinese foreign minister Wang Yi in Delhi in August 2025, India sought assurances from China regarding the removal of export curbs on products such as fertilisers and REEs (Mohan 2025). However, these discussions yielded neither any commitment nor follow-up action from Beijing. There is a realisation within the Indian government that in the short to medium term, it will have to rely on China for components, machinery and technology. Plans are afoot to ease visa norms for Chinese nationals in non-technical executive roles within Chinese companies operating in India (Mukherjee and Chaudhury 2025). This is a U-turn from the government’s position to completely Indianise the operations of Chinese companies by only having Indian nationals in major management roles.

The ‘normalisation’ of relations post-Galwan, and the pace at which it is unfolding, are neither on India’s terms nor determined by it (Jacob 2025). Questions of market access for Indian products in China and the continued prevalence of non-tariff barriers remain unresolved, with no positive signals from Beijing of accommodating India’s concerns. While Apple has big plans for India (Milmo 2025), the steady stream of media announcements on US tariffs suggests that matters are complicated. For all its diversification plans, the company still retains its main production lines in China and has not announced any plans to move out of the country. In this context, political rhetoric needs to be tempered with reality (Goyal 2025). As Patrick McGee argues in Apple in China: The Capture of the World’s Greatest Company, much of Apple’s operations in India are still confined to ‘final assembly, test, and pack out’, with components shipped from China (2025: 366).

Long-Term Initiatives to Reduce Dependence

India’s focused attention on electronics component manufacturing (ECMS) (Press Information Bureau 2025a) began only in March 2025, when the cabinet approved a scheme worth ₹22,919 crore (US$2.59 billion) over six years, to promote self-reliance in the electronics supply chain. The scheme targets five segments: (a) sub-assembly (display and camera modules); (b) bare components (including printed circuit boards and lithium-ion cells); (c) select bare components (like resistors, capacitors, and inductors in surface mount devices); (d) supply chain ecosystem and capital equipment; and (e) telecom sub-assembly. The fiscal incentives are divided into two categories based on turnover in target segment products: a turnover-linked incentive (with a period of six years, including one-year gestation period), and a capex incentive (with a period of five years). The scheme seeks to expand domestic value addition and create a robust ecosystem with the aim of attracting investments of ₹59,350 crore (US$6.69 billion), targeting production worth ₹4,56,500 crore (US$51.46 billion), and projecting direct employment for over 1,42,000 individuals.

The government claims to have received 249 applications across four segments, with the supply chain ecosystem and capital equipment segment open until May 2027. Over Financial Year 2025-26, across three tranches, the government has approved 46 ECMS projects across 11 Indian states (Press Information Bureau 2026a). Some applications involve JVs between Indian and Chinese contract manufacturers. The central government has greenlit some proposals involving JVs between Indian and Chinese electronics companies (Singh 2025). However, its insistence that Chinese partners hold lower equity in JVs complicates such arrangements. Chinese companies have been reluctant to engage in low-stakes partnerships and remain non-committal about knowledge and technology transfer. While presenting the Union Budget 2026–27, Finance Minister, Nirmala Sitharaman announced an expansion of outlay for ECMS to ₹40,000 crore (US$4.4 billion) (2026).

At the same time, there is no evidence of any Chinese company participating in the PLI scheme for mobile manufacturing, where the lion’s share of incentives has been garnered by Apple’s contract manufacturers (Barik 2025). The efficacy of the PLI scheme itself has come under scrutiny: on the one hand, there has been no value addition by foreign companies, and on the other, Indian firms have been found wanting in terms of upgrading to sophisticated manufacturing capabilities (Iyer 2025). Another long-term initiative towards self-sufficiency is the ₹1,500 crore (US$165 million) incentive scheme to develop domestic recycling capacity for the separation and production of critical minerals from secondary sources. Introduced under the National Critical Minerals Mission (Ministry of Mines 2025a), the scheme has a tenure of six years from FY 2025–26 to FY 2030–31. Eligible feedstock includes e-waste, lithium-ion battery scrap, and other scrap like catalytic convertors in end-of-life vehicles (Ministry of Mines 2025b). While India has been making efforts to future-proof its position in the critical minerals sector (Khadka 2024; Press Information Bureau 2025c; Sinh and Xavier 2025), the technological landscape is also gradually moving away from REEs and towards building alternative working models aimed at reducing dependence on Chinese-dominated supply chains. (Baid and Kotasthane 2025).

Need for Economic-Administrative Reforms in India

The Donald Trump administration’s imposition of 50 per cent tariffs on India has been seen as a key factor speeding up India’s re-alignment with China, as reflected in Prime Minister Modi’s meeting with Xi Jinping on the sidelines of the Shanghai Cooperation Organisation Summit in Tianjin in September 2025. It is important not to solely attribute the renewed engagement to the tariffs, as dialogue and meetings had gathered pace after the conclusion of the Patrolling Agreement on Eastern Ladakh in October 2024. After all, in 2023, it was Indian External Affairs Minister S. Jaishankar who snapped at fellow Indians raising questions about the government’s competence in handling the China challenge by asking on television, ‘What am I going to do? As a smaller economy, am I going to pick a fight with the bigger economy?’ (2023).

That narrow focus on China’s economic size was notably absent when the Government of India imposed restrictions on Chinese trade and investment in April 2020—encapsulated in what is known as Press Note 3. However, Jaishankar’s later admission of weakness probably gave China the upper hand in later diplomatic parleys.

In any case, India’s own economic weaknesses, and the inability of its businesses to make long-term strategic choices at the cost of short-term pain, have meant that, despite frequent calls for atmanirbharta, opportunities to build capacity have been squandered. While international circumstances have played a role, the Indian government’s economic policies are no less to blame. There is little to no ‘cooperative federalism’ in practice, and states—which should be the engines of growth in a large country like India—are unable to perform effectively. Excessive centralisation, both at the central and state levels, coupled with poor flows of bank credit and an ill-conceived PLI scheme, has reduced economic dynamism and curtailed the initiative and risk-taking ability necessary to boost productivity and growth.

Just as importantly, India’s industrial titans have underinvested in R&D, which is critical for pushing the country to the frontiers of technology. Chinese private companies account for 77 per cent of gross expenditure on R&D while Indian private companies account for only 36.4 per cent, most of which is directed toward biotechnology and IT (Department of Economic Affairs 2025). Whatever the degree of centralisation or authoritarianism in China, there is no shortage of willingness to bet on new ideas and technology with money as well as a long rope. The Chinese understand the value of gaining asymmetric advantages through leaps in technology, as demonstrated by the DeepSeek AI tool.

Meanwhile, the belief held by NITI Aayog and Indian industry that economic opportunities will beckon if India and China can agree to work together is well-intentioned but misplaced. It stems from an ignorance of the Chinese political economy. Ask Indian industry to define what a ‘private’ company is in China, or to explain what constitutes ‘profit’ for a Chinese enterprise, and they are unlikely to do so correctly.

None of the conditions that led to Press Note 3 have changed, but it is also time to stop blaming the Indian government for all the ills in its China policy. Indian industry has simply not pulled its weight or made the right investments or choices. The Chinese Party-state ensures that the so-called ‘private sector’ does its bidding even as it allows firms the flexibility and nimbleness usually associated with private enterprise. The US CBP’s actions on Indian solar PV modules highlight the need for Indian companies to remain plugged into the complexities and dynamics of Chinese domestic politics. The inability of Indian companies to track the locations within China from where raw materials and components are sourced illustrates the need for more focused and deeper assessments of China by India Inc. In fact, reliance on consultancies, especially foreign ones, rather than funding homegrown research on China, is creating a new set of long-term problems. Though ambitious, increased emphasis on export-led manufacturing, coupled with growing geopolitical headwinds, requires Indian companies to be far more aware of developments within China and to act accordingly.

NITI Aayog has advocated that India ‘plug itself into China’s supply chain’ to boost manufacturing, proposing that Chinese companies be allowed to take up to a 24 per cent stake in Indian firms without security clearance. What explains the figure of 24 per cent? Why would foreign companies invest without a controlling stake, especially in a market as notoriously difficult for business as India?

The saving grace is that it is not only India that needs Chinese investments; China also needs access to the Indian market. Its manufacturing overcapacity is a serious economic weakness, and deflationary pressures loom unless Chinese enterprises can gain access to large, growing markets like India’s. Despite past missteps in foreign and economic policy, New Delhi still has the opportunity to turn things around. This will involve walking the talk on cooperative federalism, incentivising Indian companies to invest in R&D, and pushing Indian banks to actively lend to small and medium enterprises. Without active economic and administrative reforms, India’s China policy will continue to be constrained by the existing military and economic balance of power in China’s favour.

India and China: Joined at the Hip via Labour